If you want to see how leftist economic thinking has contributed to the financial and economic morass into which our nation has plunged, read an essay entitled “The Washington Post’s Debt Cult” by a man named Dean Baker, who is founder and president of a leftist think tank named the “Center for Economic and Policy Research.”

Baker takes the Washington Post to task for expressing concern about the federal government’s soaring debt. Now, when a leftist newspaper like the Washington Post is expressing concern about the federal government’s debt level, that should be enough to raise eyebrows, even among people who love out-of-control welfare-warfare state spending.

Not Baker. He isn’t concerned at all. He writes:

The Washington Post is always [sic] telling us that debt, especially government debt is bad, very bad. It’s not quite sure why or how, but debt is definitely bad.

He says that people who express concern about the federal government’s ever-increasing debt are in a “debt cult.” After all, he says, the United States is a rich country and the U.S. dollar is the world’s “reserve currency.”

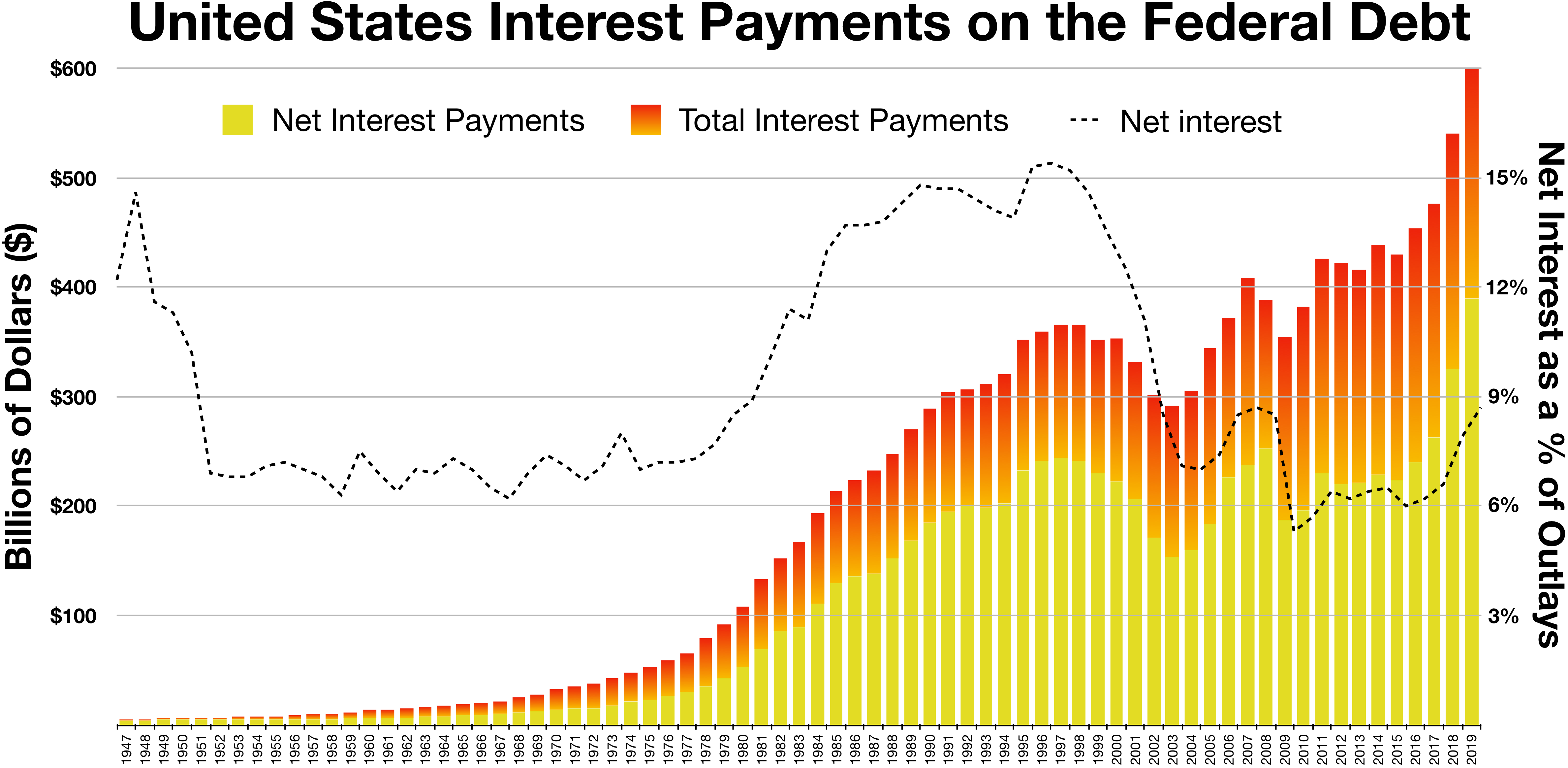

He writes, “The standard economics argument against the problem of high deficit and debt is that it will lead to higher interest rates.”

I don’t know where Baker gets his “standard” from but that’s not my argument. My argument is that high deficits and debt lead to impoverishment and even bankruptcy, both of which should concern anyone who would like to have financial and economic stability and ever-increasing standards of living.

Near the end of his piece, Baker suggests that mounting household debt is also no big deal because the “financial obligation ration,” which “measures debt payments and rent relative to income, is near a four decade low.”

He continues with a fascinating sentence: “It’s true that many people may face eviction or foreclosure in the months ahead, but that will be because they have lost their jobs, not because of high debt burdens.”

But pray tell, Mr. Baker: What do you expect these people to do about those high debt burdens once they have lost their jobs?

Permit me to explain to this leftist what the problem is with respect to soaring spending and debt.

Household spending and debt

Suppose that for the past ten years ago, the Smith family, which has four kids, has had an annual income of $50,000. Its annual expenditures, including mortgage payments, food, automobile, clothing, healthcare, and credit card debt have been $35,000. To fund its welfare-warfare state, the federal government collects $15,000 every year in taxes from the Smiths.

In other words, for the past 10 years, the Smith family has been spending 100 percent of its income. No savings at all to help get them through a month or two of unemployment.

Starting 10 years ago and continuing every year thereafter, the Smith family made it a point to go on vacation in the south of France, staying at five-star resorts. Each vacation totaled $20,000, which the Smiths charged on their Visa card. Today, the Smiths owe $200,000 on their credit card. Since all of their $50,000 annual income is committed, there is no way that they can pay down any of the principal on their Visa debt.

Nonetheless, Visa requires the Smiths to pay at least a portion of the principal each month plus accrued interest. For 10 years, they have been able to do that with their $50,000 in income by cutting down on food expenses.

However, having read one of Dean Baker’s articles, in January they went on another $20,000 European vacation and simply charged it to their credit card. That lifted their Visa debt to $220,000. When the next monthly credit card bill came in, they realized that they lacked the funds to pay the required minimum payment on the debt and the accrued interest on the debt.

What would Dean Baker say to the Smiths? “Oh, don’t worry. Everything is fine. The national ‘financial obligation ratio’ is still in positive territory. Don’t become a member of the debt cult. Be happy!”

But the reality is that Visa wants its money. it will start with letters and then proceed to telephone calls. Then, when those things don’t work, the entire debt will be accelerated and Visa will demand its entire $220,000. The Smiths, of course, don’t have $220,000. They don’t have anything saved up. (It’s worth noting that if there had been no income tax, they would have $150,000 in the bank, and that would certainly have induced Visa to extend payment on the balance.) Visa ends up filing suit for the principal, accrued interest, and attorney’s fees. Once Visa gets a court judgment, it will do everything it can to recover its money. The Smiths will have to decide whether to live with that court judgment hanging over their heads or simply declare bankruptcy and get the debt wiped away.

Federal spending and debt

The situation is really no different with the federal government, except for the fact that it really isn’t the federal government that ultimately is responsible for payment of its debts. Oh sure, in a technical sense it is because it’s the borrower. But keep in mind where the government gets its money — from taxpayers. Thus, when the government’s debts come due, it’s got to levy taxes on the American people to pay its debts.That includes, of course, the Smith family, who are quite surprised to learn that they now owe even more money. Today, each taxpayer’s share of the federal government’s debt is almost $200,000.

Before the coronavirus hit, the federal debt was $23 trillion, with each taxpayer’s share being $200,000. U.S. officials were spending $1 trillion more than what they were bringing in with taxes. That meant that the federal debt would increase to $24 trillion. With the $2 trillion dollars in additional spending owing to the coronavirus crisis, that will increase the debt to $26 trillion. With the additional $4 trillion that U.S. officials are planning to spend this year to deal with the crisis, that will mean $30 trillion in debt.

In fact, it’s a virtual certainly that it will be more that. Why? Because millions of people are now unemployed and, therefore, won’t be paying income taxes on money that they aren’t receiving. That will cause income tax revenues to plummet, which will mean even more federal debt.

Now, what happens when that $30 trillion debt comes due and the federal government can’t cover principal owed plus accrued interest because tax revenues are too low. Creditors are no different than VIsa. They want their principal and interest. They are entitled to it under the terms of their loan agreements with the federal government.

No problem, at least according to Dean Baker. The federal government simply taxes people, including the Smith Family, to get the money to pay off its creditors.

Well, except for one thing. The Smith Family and millions of other Americans don’t have any money to seize. You can’t squeeze blood out of a turnip. The feds will end up taxing and seizing everything they can find, including retirement accounts, but it still won’t be enough. Once the federal government can’t pay its bills, the gig will be up. The impoverishment of the nation will be the result, just like it was in Greece a few years ago.

But as Dean Baker says, don’t worry, be happy. Go on another $20,000 European vacation. Encourage U.S. officials to continue their welfare-warfare state spending and debt binge. Tell Visa and U.S. bondholders to lighten up and lay off. The national “financial obligation ratio” is still good. There is light at the end of the tunnel, and, don’t worry, it’s not a train heading toward you.